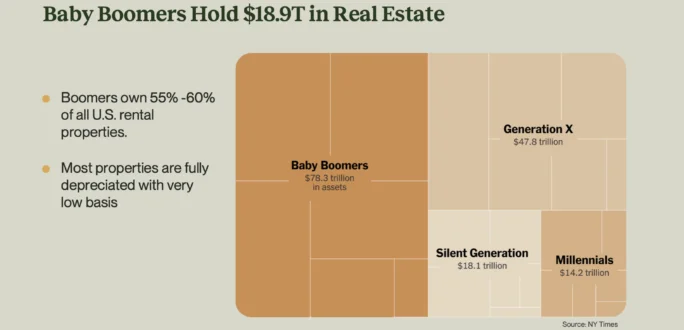

Company News

Hamilton Zanze CEO Shares Multifamily Insights and 2025 Outlook

Kurt Houtkooper was recently interviewed by Multifamily Executive magazine, discussing real estate market trends, investment strategies, and how the firm is positioning for growth in today’s environment.

Owner-operator Hamilton Zanze has sponsored the acquisition of over $6.9 billion in multifamily assets primarily in the Western, Southwestern, and Eastern United States since its founding in 2001. The San Francisco-based multifamily real estate investment firm’s portfolio comprises 122 properties with 21,326 units across 28 markets.

CEO Kurt Houtkooper oversees the overall strategic direction of the firm and is responsible for developing and executing its investment objectives. He has a primary role in building the acquisition and disposition strategy and forming relationships with family offices and institutional partners. Multifamily Executive caught up with Houtkooper to discuss what’s in store for the firm and the multifamily industry in 2025.

How do you think the multifamily industry has performed so far in 2024 when it comes to operating fundamentals, and what may be in store as we head into 2025?

Clearly there has been an oversupply issue in many markets as a result of the delivery of new construction in recent years. Some of the markets that we’re in—Colorado Springs, Colorado; Austin, Texas; and Phoenix—have been dealing with this issue, and you see occupancy challenges and rent decreases in those areas. In some bigger cities, you see the wave of new high-rise apartment buildings having similar impacts. Also, Class C communities are experiencing significant rent decreases in some cases.

At Hamilton Zanze, our portfolio consists largely of workforce housing, core-plus assets, and suburban garden-style communities, and those types of properties have not been as impacted by new supply. We also don’t have Class C assets in our portfolio.

Overall, we’re happy with how our portfolio has performed this year. Our top-line revenue growth has been 1%, and our overall occupancy rate has decreased but not by much—about 50 basis points. We’re currently at about 93.7% occupancy across our portfolio. We’ve experienced higher renewal rents per square foot than new-lease rents per square foot. As we’re putting together our budgets for 2025, we feel really good about this winter and next year. We’re anticipating higher growth in same-store sales and higher occupancy levels.

As for the industry as a whole in 2025, some headwinds will remain in oversupplied markets. But with new construction slowing, we expect really strong operating fundamentals in 2026 and 2027.

How would you characterize the pace of investment sales in 2024, and has that pace been in line with your expectations? What do you expect for next year?

2024 was another very slow year for investment sales of apartment buildings, just as we anticipated. Interestingly enough, there were some large portfolio acquisitions this year, where some of the big money—the least expensive capital—was able to deploy.

For 2025, I expect a much larger volume of investment sales and more opportunities to buy. That’s because we now have an easing monetary policy, and we know what the cost of capital is going to be on the debt side. An easing monetary policy from the Fed results in more capital being deployed, and equity is more willing to take risks. Essentially, more equity will be deployed in 2025 now that we know the direction of interest rates.

Also, I envision more ground-up developers entering the value-add space and becoming buyers of existing product, and I see investors that previously focused upon office buildings now buying apartment buildings. When you have this much competition and this much capital going toward one segment of the real estate asset class, you’re going to have cap-rate compression.

How would you summarize your company’s priorities and activities in 2024, and do you see that changing in 2025?

We had two major initiatives in 2024 that we think will position us well for 2025 and beyond.

The first was the launch of our Evergreen Fund. We are contributing existing stand-alone assets into the diversified portfolio fund using tax code 721.

We also started a new company focused on rent-control housing in California, through which we’re looking to purchase distressed real estate and notes in San Francisco and Los Angeles. We recently executed our first large transaction in San Francisco and expect more in 2025.

These two major initiatives will continue to be major points of emphasis for us in 2025.

Can you tell us more about the HZ Evergreen Fund’s benefits and impact?

The fund represents our evolution and our ongoing commitment to positioning our investors to achieve both their short- and long-term financial goals.

Initially, we’re focusing on properties within our existing portfolio that fit the fund’s criteria, with a plan to transition them into the fund by 2026. We have identified 50 apartment communities across 22 metropolitan areas to be included.

These assets, currently owned by exchange capital—either in a Delaware Statutory Trust or a tenancy-in-common—are being transitioned from single, stand-alone entities into a diversified vehicle.

One of the key benefits for investors is estate planning, as shares can be easily transferred among family members. The fund also offers geographic diversification, liquidity, access to lower-cost capital, and improved debt options. Additionally, it provides a more predictable and durable income stream, as investors are not dependent on the performance of a single asset, but on a large portfolio of communities.

Looking ahead, the 1031 exchange program remains a vital tool for real estate investors but has historically been part of discussions during major tax reform efforts, with occasional proposals to limit or eliminate it. While the program is currently intact, its future is never guaranteed, given its periodic scrutiny. In the event of adverse changes to the 1031 exchange, the Evergreen Fund offers an excellent alternative for exchange capital, providing investors with a reliable solution in an evolving tax landscape.

What tailwinds do you think the multifamily industry will face in 2025?

Obviously, there were challenges over the past couple years in terms of rising interest rates, but we think that we’re going to see a decrease in rates in 2025. That will hopefully be accompanied by an increase in the valuations of apartment buildings and a noticeable uptick in investment sales and acquisition opportunities.

On the flip side, what headwinds will it encounter next year?

Number one, a lot of supply remains in certain submarkets, so oversupply is going to continue to be a challenge next year. Number two, as operators we are always concerned about any new regulations, such as new forms of rent control that might arrive in the markets that we’re in.

What is one trend you’re watching that could disrupt the multifamily industry?

I think that the private REITs and evergreen funds could signal a massive shift in the industry. They offer liquidity, indexing, and limited fees. The future of those types of vehicles will be very attractive to capital, and, as capital seeks to find those types of vehicles, it could be very disruptive to public REITs.

Company News

Hamilton Zanze CEO Kurt Houtkooper joins Multi-Housing News to discuss the momentum building in multifamily in 2026.

Read

Company News

Press Releases

Award recognizes his impact on portfolio growth and his devoted mentorship.

Read

Company News

HZ President and CIO David Nelson breaks down why Reno is one of the strongest apartment markets in the country.

Read